Isabella Gollini*, Birkbeck, University of London

Jonathan Rougier, University of Bristol

*This research was developed while Isabella Gollini was on a postdoctoral fellowship in the CREDIBLE project at the University of Bristol

DOWNLOAD

THE CHALLENGE

The main aim of this project was to evaluate the risk of insolvency, as the probability that the annual loss will exceed the company’s current operating capital.

One of the objectives in catastrophe modelling is to assess the probability distribution of losses for a specified period, such as a year. From the point of view of an insurance company, the whole of the loss distribution is interesting, and valuable in determining insurance premiums. But the shape of the right hand tail is critical, because it impinges on the solvency of the company. A simple measure of the risk of insolvency is the probability that the annual loss will exceed the company’s current operating capital. Ensuring an upper limit on this probability is one of the objectives of the EU Solvency II directive.

WHAT WAS ACHIEVED

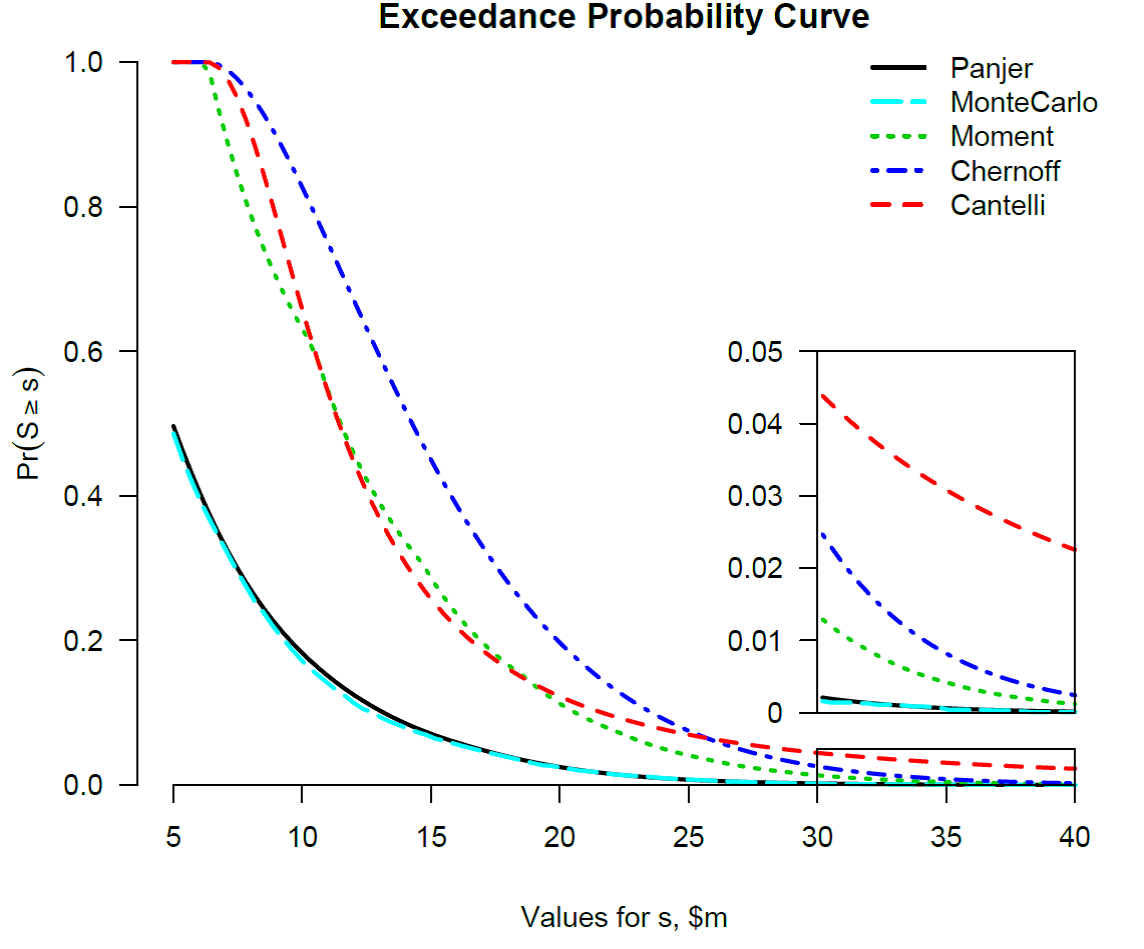

Using results from Probability Theory, we derived four upper bounds and two approximations for the upper tail of the loss distribution that follows from an Event Loss Table. We argue that in many situations an upper bound on this probability is sufficient. For example: to satisfy the regulator, in a sensitivity analysis, or when there is supporting evidence that the bound is quite tight. Of the upper bounds we have considered, we find that the Moment bound offers the best blend of tightness and computational efficiency. In fact, the Moment bound is effectively costless to compute, based on the timings from our R package.

HOW WE DID IT

What did you do during the project to deliver its achievements and outcomes? This section can be more technical but it doesn’t have to be. You can include additional images or diagrams if you wish. Avoid using jargon and acronyms. What will interest the reader and a wide audience of people? (180-280 words depending on the use of diagrams, images or figures)

We explored six different approaches to evaluate the annual loss distribution: Monte Carlo simulation and Panjer recursion, both of which are widely used but also very computationally expensive, and four upper bounds which are effectively costless to compute. We demonstrated the conditions under which the upper bounds are tight, and the appropriate size for Monte Carlo simulations. We presented a numerical illustration of all the methods proposed using a large Event Loss Table (with 32,060 events) concerning US hurricane data, and used this challenging application to assess the various methods, carried out in our ‘tailloss’ package for the R computing environment.

REFERENCE OR LINKS

Gollini, I., and Rougier, J., (in press) “Rapidly Bounding the Exceedance Probabilities of High Aggregate Losses”, The Journal of Operational Risk. Preprint: http://arxiv.org/abs/1507.01853

Gollini, I., and Rougier, J., (2015) “Tailloss: An R package to Estimate the Probability in the Upper Tail of the Aggregate Loss Distribution” https://cran.r-project.org/web/packages/tailloss/index.html

http://www.risk.net/type/journal/source/journal-of-operational-risk